Germany is moving toward a fully digital invoicing model, with obligations that already apply to transactions between businesses and public authorities (B2G), as well as to transactions between businesses (B2B). The electronic invoicing framework is overseen by the German Federal Ministry of Finance (BMF).

Business‑to‑consumer (B2C) transactions are not affected by this national mandate. In addition, for now, cross‑border and intra‑EU operations are not covered (without prejudice to future ViDA requirements).

E‑invoicing for the German public administration

In the public sector, Germany uses a centralized system in which all public administrations receive electronic invoices through standardized infrastructures.

The Bund (federal level) and many public entities receive e‑invoices through platforms such as ZRE/OZG‑RE and/or via Peppol, while in the Länder (federal states) the specific portals or channels may vary depending on the administration.

The most commonly used formats are XRechnung, Peppol BIS (via Peppol) and, in certain cases, ZUGFeRD.

Electronic invoicing is mandatory for all B2G transactions.

German B2B model: how e‑invoicing works

The obligation for B2B transactions generally applies to operations between “inländische” entrepreneurs, that is, companies with their registered office, place of management or establishment in Germany. There are some exceptions, such as certain transport tickets that function as invoices, among others.

Regarding the validation system, the B2B model is based on a post‑audit approach, which means:

- Invoices do not pass through any government platform before being sent.

- There is no prior automatic validation; each company is responsible for issuing and receiving compliant invoices.

- Documentation must remain complete, authentic, and readable for any future verification.

- The tax administration may conduct audits afterwards to ensure that invoices meet all requirements.

This model offers flexibility, but also means that companies must have:

- Systems capable of issuing and receiving structured formats compliant with EN 16931 (UBL, CII or ZUGFeRD EN‑compliant).

- Robust internal processes to guarantee document quality.

- Secure archiving methods to demonstrate compliance in the event of a review.

In short, for B2B transactions, there is no government validation at the time the invoice is sent; compliance depends entirely on the company.

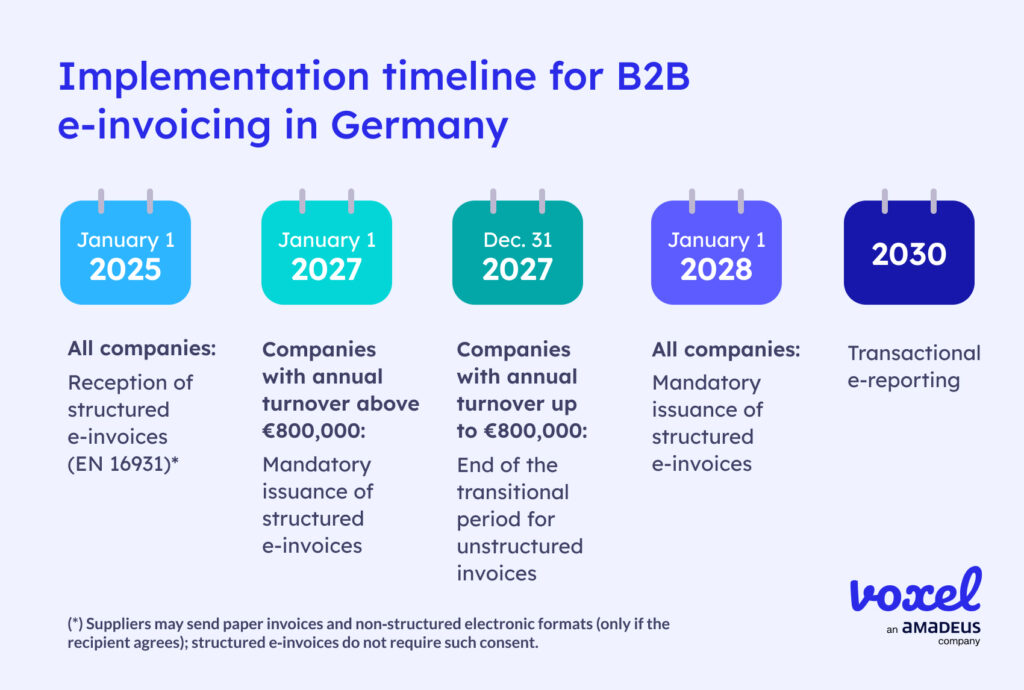

B2B e‑invoicing timeline in Germany

The planned timeline for the entry into force of mandatory e-invoicing between businesses is as follows:

From 01/01/2025 – Already in effect.

Companies must be able to receive structured electronic invoices (EN 16931). Suppliers may continue sending paper invoices and non‑structured electronic formats such as PDF (only if the recipient agrees). Consent from the recipient is not required for issuing structured e‑invoices.

From 01/01/2027 – Companies with annual turnover above €800,000.

Businesses exceeding €800,000 in annual turnover will be required to issue structured e‑invoices. Invoices issued via direct system‑to‑system exchange will remain valid as long as they comply with the standard and both parties agree.

Until 31/12/2027 – Companies with annual turnover equal to or below €800,000.

From 01/01/2028 – All companies.

The obligation extends to all businesses, regardless of size. This marks the end of paper and non‑structured documents (PDF), and the start of mandatory issuance of structured electronic invoices.

Around 2030.

Germany will introduce a transactional electronic reporting system aligned with the EU’s ViDA initiative.

How can German companies prepare for B2B e‑invoicing?

To comply with the regulation, companies must ensure that their systems are capable of receiving and issuing structured electronic invoices in line with the European standard EN 16931.

Voxel ensures full legal compliance in Germany, supporting companies in adapting their systems and processes in a secure, scalable way, aligned with current and future regulatory requirements.

Complete the form below if you would like to speak with our team of experts and receive tailored advice to prepare your company for e‑invoicing in Germany.