October 1, 2026 marks the start of the mandatory application of electronic invoicing in B2B relationships in Spain, with a progressive implementation schedule depending on the type of company.

The publication of Royal Decree 238/2026 represents a decisive step toward the implementation of mandatory electronic invoicing in B2B relationships in Spain. The regulation develops the mandate set out in the “Crea y Crece” Law and lays the foundations of the new Spanish electronic invoicing system.

The Royal Decree specifies three key obligations: the issuance, transmission, and receipt of electronic invoices in the B2B environment; the obligation for the recipient to report the status of invoices; and the obligation, also on the recipient’s side, to report the status of payments.

From legal approval to practical implementation

The Royal Decree has already been approved and the draft Ministerial Order has been published. The latter establishes the key dates for the mandatory implementation of electronic invoicing (detailed in the following sections) and includes the general technical parameters as well as certain specifications of the public electronic invoicing solution.

In a subsequent phase, from draft to publication of the Ministerial Order in the Official State Gazette (BOE), this Order will mark the final step and will be responsible for:

- Defining the technical parameters and specifications of the public electronic invoicing solution.

- Detailing the interfaces, services, authentication mechanisms, and operational rules of the system.

- Establishing any other technical aspects not defined in the Royal Decree itself.

Mandatory electronic invoicing: who it applies to

Mandatory electronic invoicing applies exclusively to B2B transactions between companies and professionals that are required to issue invoices under Spanish regulations when:

- The recipient is established in Spain.

- Or the recipient has a permanent establishment, domicile, or habitual residence in Spain and the transaction is linked to that establishment.

The regulation does not apply to simplified invoices; regulated electricity and gas markets; or IATA invoicing (BSP, CASS, and SIS‑ICH).

Electronic B2B invoicing implementation timetable in Spain

The implementation schedule will enter into force on October 1, 2026. In addition to electronic invoicing, it includes obligations to report the status of invoices and payments. For companies, this is structured as follows:

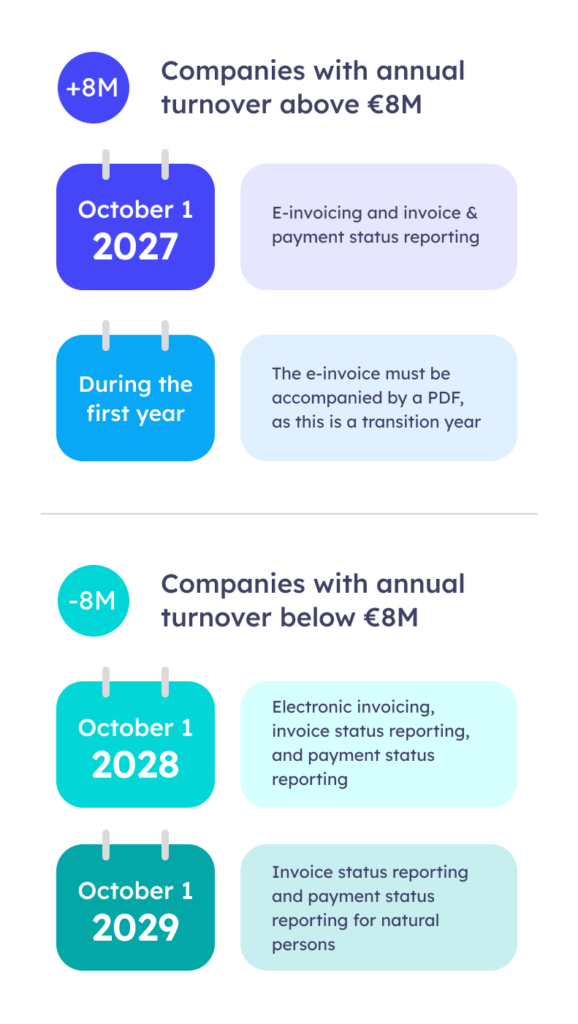

October 1, 2027 – Companies with annual turnover > €8M

- Electronic invoicing, invoice status reporting, and payment status reporting.

- During the first year of mandatory electronic invoicing, the e‑invoice must be accompanied by a PDF, as this is considered a transition period.

October 1, 2028 – Companies with annual turnover < €8M

- Electronic invoicing.

- Invoice status and payment status reporting.

- For individuals (mainly self‑employed professionals), these two reporting obligations will become mandatory as of October 1, 2029.

Other information of interest

- B2B invoices must be issued exclusively in a structured electronic format. Accepted formats include UBL, CII, Facturae, and EDIFACT.

- The mandatory public repository will only accept the UBL format and must contain a faithful copy of each invoice.

- The invoice recipient must always report the effective payment of the invoice, including the actual payment date. This information must be communicated directly to the public electronic invoicing solution. The issuer may report the payment voluntarily, but the obligation lies with the recipient.

- The publication of Royal Decree 238/2026 does not directly affect the Verifactu regime. The two regimes will coexist.

- Alignment with the European ViDA (VAT in the Digital Age) regulation.

How the Spanish electronic invoicing system works

The issuance and receipt of invoices, as well as the notification of statuses, will be carried out through the Spanish electronic invoicing system. This system is composed of the public electronic invoicing solution, private electronic invoicing exchange platforms (PIFEs), and the company.

The process will follow these steps:

- The issuing company’s PIFE will send B2B invoices.

- The PIFE must also send a faithful copy of the invoice, in UBL format, to the public solution, which will act as a repository.

- The recipient must communicate acceptance or rejection of the invoice within a maximum of 4 calendar days from when that status occurs, and must also report payment within a maximum of 4 calendar days from the effective receipt of funds. These are independent timeframes.

Next steps

From now on, companies, technology providers, and public authorities will need to work in a coordinated manner to turn the regulatory framework into an operational reality.

At Voxel, we are working to ensure that the Bavel platform meets the necessary technical requirements, guaranteeing that our clients are always aligned with current regulations.

If you would like us to help you comply with Spain’s B2B electronic invoicing regulations or if you have any questions, please contact us at info@voxelgroup.net.